He that is of the opinion money will do everything may well be suspected of doing everything for money.

— Benjamin Franklin

A dollar is a dollar, right? Setting aside rare collectibles, of course, and assuming they’re both in spendable condition, a particular dollar is worth as much as any other, right? Surely that must be true. Our entire monetary system is based on it. It’s what money is for, really — to provide a uniform medium of exchange.

Except it isn’t true. I’ll prove it to you.

The Value of $1 Million

Let’s say you woke up in the morning, checked your bank account balance, and found an extra million dollars had been added. Tax free, legal, nothing shady going on, no strings attached. How valuable would that be for you? How would that make you feel? What effect would it have on your life? What would you be willing to do to make that happen?

The median individual American would have to work for forty years just to earn that much money, and that’s before deducting a single cent of living expenses. Imagine it — the fruits of an entire working career, in an instant. How would you react?

Now imagine how Warren Buffett would react if the same thing happened to him. I can’t say for sure, but I imagine he would say something along the lines of, “Oh, is it Thursday already? This week has flown by.”

The truth is that the value of a dollar in terms of overall human welfare changes enormously based on whose hands it lands in, and depends a great deal on how much money the person already has. If you’re broke, in debt, and being hounded by hyper-agressive collection agencies, $1 million dollars would change your life. If you’re a billionaire, however, it’s a rounding error. You probably gain and lose millions of dollars before lunch every day from market fluctuations.

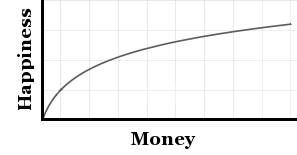

In other words, for my fellow nerds,1 money has roughly logarithmic value:

Those first few dollars you save after getting out of debt feel really, really good. But once you have a good cushion built up, your monthly contribution doesn’t bring in quite as much joy as it once did. Importantly, blowing it on something frivolous doesn’t hurt as much as it once did, either.

A Double-Edged Sword

This effect can be insidious if you’re not careful. It can lead to you sabotaging your progress just when you’re starting to build some real momentum. That tempting new toy you’ve been eyeing for a while might start to look like it will bring more satisfaction than a few hundred more dollars in your already respectable brokerage account. Beware!

It can also set you free, however — once you discover that the graph is pretty flat once you hit financial independence. At that point, growing richer isn’t likely to make you all that much happier. Realizing this can help you give yourself permission to let go of the grind.

A Story to Reflect On

Legend has it that Kurt Vonnegut and his friend Joseph Heller once attended a party at the house of a billionaire hedge fund manager. Vonnegut noted that their host had made more money in one day than Heller ever made from his most famous novel, Catch-22. 2

Heller responded, “Yes, but I have something he will never have: enough.”

5 Comments